What You Think You Know About Reverse Mortgages Is Probably Wrong

For years, reverse mortgages have been surrounded by myths, misinformation, and outdated opinions. Unfortunately, many homeowners dismiss them based on something they heard decades ago from a friend, a family member, or even a television commercial.

I am here to provide you the facts. I have been teaching retirees, Realtors, Loan Officers, and financial planners the real information about reverse mortgages for years. Hi, my name is Richard Woodward, a certified reverse mortgage specialist with over 20 years of experience. I have access to more reverse mortgage lenders than any other company in the United States.

The truth is that today’s reverse mortgage is very different than the one many people remember. If you would like to read all about reverse mortgages, here is a link to HUD, the administer of the FHA insured Reverse mortgage. You can read it for yourself, or if you stick with me, I will break down the myths.

- Official HUD Policy Library: HUD Single Family Housing Policy Handbook (4000.1)

Reveres mortgage rules:

To really have knowledge, it’s helpful to know that Section II.B of the handbook covers the core HECM rules:

- II.B.1 & II.B.2: Origination, counseling, and processing requirements.

- II.B.4: Underwriting the property (appraisal standards and property eligibility).

- II.B.5: Performing the Financial Assessment of the borrower (evaluating credit history, property charge payment history, and residual income requirements).

If you’re 62 or older and own your home, it’s worth taking another look. What you think you know about reverse mortgages is probably wrong.

Myth #1: “The Bank Takes Your Home”

This is by far the biggest misconception.

A reverse mortgage does not give ownership of your home to the lender.

Just like a traditional mortgage, you remain the owner of your home. Your name stays on the title, and you continue building any additional equity as your home’s value increases.

As long as you:

- Live in the home as your primary residence

- Pay your property taxes

- Maintain homeowners insurance

- Keep the home reasonably maintained

the home remains yours. When the time comes to pay off the home, the mortgage insurance ensures you or your heir will never owe more than 95% of the appraised value at time of payoff. This mitigates all the risk. Most likely, under today’s rules and interest rates, your home equity will continue to grow for years.

A Story You May Have Heard—But Not the Whole Story

You’ve probably heard someone say, “My grandmother lost her home because she had a reverse mortgage.” Stories like this have contributed to many of the myths surrounding reverse mortgages.

But when you dig a little deeper, the real story is often very different.

For example, imagine a grandmother who obtained a reverse mortgage and lived comfortably in her home for many years without making monthly mortgage payments. Over time, she and her family stopped paying the annual property taxes. Eventually, the county placed a tax lien on the property, and after the taxes remained unpaid, the taxing authority foreclosed on the home.

It’s easy for people to conclude that the reverse mortgage caused her to lose the home. In reality, it was the failure to pay the required property taxes that led to the foreclosure.

The same outcome could have occurred if she had a traditional “forward” mortgage—or even if she owned the home free and clear with no mortgage at all. Property taxes are a responsibility of every homeowner, regardless of the type of financing they have.

Reverse mortgage borrowers are still required to:

- Pay their property taxes on time.

- Maintain homeowners insurance.

- Keep the home in reasonable repair.

- Continue using the home as their primary residence.

Meeting these obligations allows the borrower to remain in the home. The reverse mortgage itself was not the reason the home was lost; the unpaid property taxes were.

This is an important distinction because it illustrates how easily myths can spread when the full story isn’t told. Reverse mortgages don’t exempt homeowners from the normal responsibilities of homeownership—they simply eliminate the requirement to make monthly mortgage payments on the loan itself.

Myth #2: “My Children Will Lose Their Inheritance”

Many people believe their children won’t receive anything when they pass away.

In reality, your heirs have several options:

- Sell the home and keep any remaining equity after the loan is paid off.

- Refinance the reverse mortgage into a traditional loan if they want to keep the home.

- Refinance the home for 95% of its current appraised value, even if the loan balance is higher than the home’s value (thanks to FHA rules).

Because reverse mortgages are non-recourse loans, neither your heirs nor your estate will ever owe more than the home’s value.

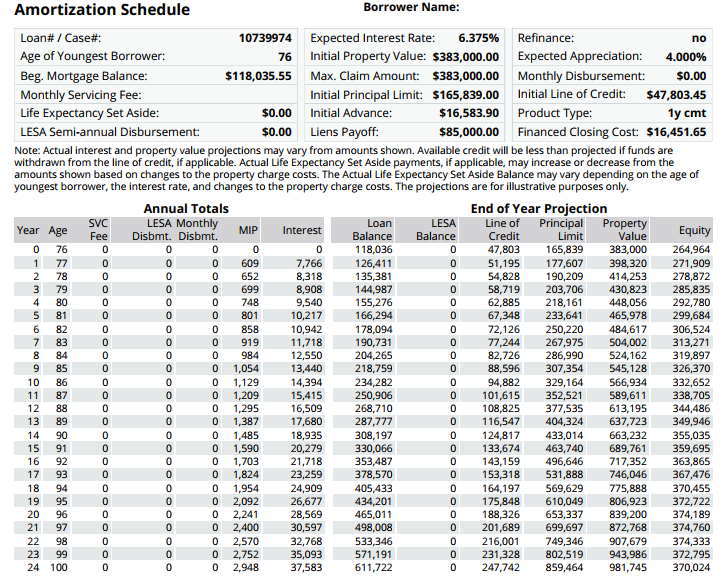

Take a look at a typical amortization schedule for a proposal. Notice the equity continues to grow over time at current rates. However, each borrower is different, and I am happy to provide your custom amortization schedule.

Myth #3: “I’ll Owe Monthly Mortgage Payments”

One of the biggest advantages of a reverse mortgage is exactly the opposite.

With a Home Equity Conversion Mortgage (HECM), there are no required monthly mortgage payments as long as you continue meeting the loan obligations.

Instead of writing a mortgage payment every month, many homeowners improve their monthly cash flow and reduce financial stress. However, you can customize your financial situation if you like by making any payment you like. It is not a one-size-fits-all program.

Myth #4: “I’m Giving Up All My Equity”

Absolutely not.

Many homeowners continue to have substantial equity for years after obtaining a reverse mortgage.

Your remaining equity depends on factors like:

- Home appreciation

- How much money you borrow

- Interest rates

- How long you remain in the home

In many markets—including North Texas—home values have appreciated significantly over time, allowing many reverse mortgage borrowers to retain considerable equity.

Myth #5: “Reverse Mortgages Are Only for People Who Are Broke”

This may have been true years ago, but today many financially successful retirees use reverse mortgages as part of a comprehensive retirement strategy.

Financial planners often recommend reverse mortgages to:

- Delay taking Social Security benefits

- Reduce withdrawals from retirement accounts during market downturns

- Create a standby line of credit for emergencies

- Eliminate monthly mortgage payments

- Preserve investment portfolios

- Increase retirement cash flow

Many homeowners use a reverse mortgage because it’s a smart financial tool—not because they’re struggling.

Why Financial Planners are Raving About Reverse Mortgages for Retirement

Many well-known financial planners and reverse mortgage authors have voiced their support for reverse mortgages. Here are some of their opinions:

Wade Pfau, a professor of retirement income at The American College of Financial Services, has said, “Reverse mortgages have gone from being a loan of last resort to a tool that can be used in a thoughtful, integrated retirement income plan.”

Jamie Hopkins, director of retirement research at Carson Group, has said, “Reverse mortgages are a viable solution for retirees looking to supplement their retirement income, pay off debt, or fund home repairs and renovations.”

Tom Hegna, a retirement expert and author of “Don’t Worry, Retire Happy,” has said, “A reverse mortgage is a powerful financial tool that can help retirees live the retirement they’ve always dreamed of.”

Barry Sacks, a retired tax attorney and author of “Reverse Mortgages: How to Use Reverse Mortgages to Secure Your Retirement,” has said, “Reverse mortgages have become much more flexible and affordable in recent years, making them a valuable tool for retirees.”

Myth #6: “You Can’t Buy a Home With a Reverse Mortgage”

Actually, you can.

One of the fastest-growing reverse mortgage programs is the HECM for Purchase.

Instead of paying cash for your retirement home, you can:

- Make a large down payment (typically 45–60%, depending on age and interest rates)

- Finance the remaining balance with a reverse mortgage

- Eliminate required monthly mortgage payments

- Preserve more of your retirement savings

Many retirees are using this strategy when downsizing or relocating to Texas. Read my blog post: Reverse Mortgage For Purchase

Myth #7: “Reverse Mortgages Have Crazy Fees”

Like any mortgage, there are closing costs.

However, today’s reverse mortgages are heavily regulated by the FHA, and fees are fully disclosed before closing.

In many cases, the financial benefits—such as eliminating monthly mortgage payments or accessing tax-free proceeds—can outweigh the upfront costs.

Every homeowner’s situation is different, which is why a personalized analysis is so important. I provide my clients with multiple options with different fees so they can select the best program and fee structure for them.

Myth #8: “If Home Values Drop, My Family Will Owe Money”

No.

HECM reverse mortgages are insured by the Federal Housing Administration (FHA).

This means the loan is non-recourse.

Even if home values decline dramatically, neither you nor your heirs will ever owe more than the home’s value when the loan becomes due.

That protection is one of the biggest advantages of the program.

Myth #9: “Reverse Mortgages Are Too Complicated”

They really aren’t.

A reverse mortgage works much like a traditional mortgage, except the repayment occurs when:

- You permanently move out of the home

- Sell the home

- Or the last borrower passes away

Before closing, every borrower is required to complete independent HUD-approved counseling to ensure they fully understand the program and determine whether it’s the right fit.

Who Should Consider a Reverse Mortgage?

A reverse mortgage may be worth exploring if you:

- Are age 62 or older

- Want to eliminate your monthly mortgage payment

- Need additional retirement income

- Want access to your home’s equity without selling

- Are planning for long-term retirement security

- Want to purchase a retirement home while preserving cash

- Prefer greater financial flexibility in retirement

- Want to preserve your stock market or cash assets during market down turns.

It’s not the right solution for everyone—but for the right homeowner, it can be life-changing.

The Bottom Line

Reverse mortgages have evolved significantly over the past two decades. Many of the stories you’ve heard simply don’t reflect how today’s FHA-insured reverse mortgages work.

Rather than thinking of a reverse mortgage as a “loan of last resort,” many retirees now view it as another financial planning tool—one that can help improve cash flow, preserve assets, and provide greater peace of mind.

The key is understanding the facts instead of relying on outdated myths.

Let’s Talk About Your Options

If you’re curious whether a reverse mortgage could fit into your retirement plan, I’d be happy to provide a personalized, no-obligation consultation.

Every homeowner’s situation is unique, and together we can determine whether a reverse mortgage makes sense for your goals.

Frequently Asked Questions: Reverse Mortgage Myths

Q: Can a reverse mortgage company take your home? No. As long as you live in the home as your primary residence, pay your property taxes and homeowner’s insurance, and maintain the property, a reverse mortgage lender cannot take your home. The most common reason homeowners lose a home connected to a reverse mortgage is unpaid property taxes — which would cause foreclosure with any type of mortgage or even no mortgage at all.

Q: What happens if I don’t pay property taxes on a home with a reverse mortgage? If property taxes go unpaid, the local taxing authority — not the reverse mortgage lender — can initiate foreclosure proceedings. This is the same outcome that would occur with a conventional mortgage or even a free-and-clear home with no mortgage. Unpaid property taxes are a risk of homeownership in general, not a reverse mortgage-specific risk.

Q: Do reverse mortgage companies want you to default so they can take your house? No. Reverse mortgage lenders are FHA-regulated and have no financial incentive to foreclose. In fact, HUD’s Life Expectancy Set-Aside (LESA) program was specifically created to automatically reserve funds for property taxes and insurance for borrowers who may have difficulty managing these payments on their own.

Q: Will my children inherit my reverse mortgage debt? No. Reverse mortgages are non-recourse loans, meaning your heirs can never owe more than the home is worth at the time the loan is repaid. If the loan balance exceeds the home’s value, FHA mortgage insurance covers the difference. Your children will never be asked to pay the difference out of their own pocket.

Q: Is a reverse mortgage a good idea for seniors? It depends entirely on the individual situation. Reverse mortgages work best for homeowners who plan to stay in their home long-term, have significant equity, and want to supplement retirement income or eliminate a mortgage payment. They’re less suitable for homeowners who plan to move soon or whose family has concerns about managing ongoing property obligations. An honest conversation with a licensed specialist — not a TV commercial — is the best way to find out if it’s right for you.

Q: Why do so many people say reverse mortgages are bad? Most negative reverse mortgage stories trace back to one of three causes: unpaid property taxes or insurance, a permanent move out of the home, or a lack of family planning and communication. In nearly every case, the same outcome would have occurred with a conventional mortgage or even outright homeownership. The reverse mortgage becomes the villain in the story because it’s easier to blame a financial product than to address the underlying circumstances.

Q: What is the biggest risk of a reverse mortgage? The biggest real risk is outliving your equity — borrowing against your home over many years and leaving little or nothing for your heirs. This is a legitimate consideration that every borrower should discuss openly with their family and their loan officer before moving forward. It’s not a hidden risk — it’s disclosed clearly during HUD counseling — but it deserves serious thought.

Richard Woodward

Certified Reverse Mortgage Specialist

NMLS #217454

The Richard Woodward Team | NEXA Lending

Phone: 214-945-1066

A reverse mortgage isn’t right for everyone—but making a decision based on facts instead of myths is always the right first step.